Retail banks are at a critical inflection point. After decades of investment in digitalization, many banking institutions still struggle with fragmented processes, operational inefficiencies, and ever-rising customer expectations.

A new joint report by Boston Consulting Group (BCG) and OpenAI, “How Retail Banks Can Put AI Agents to Work,” argues that the next wave of transformation will not come from incremental improvements, but from adopting AI agents capable of executing complex, end-to-end workflows.

Key findings of the report:

▪ If banks move from task-level AI copilots to agents that execute full workflows, they could achieve profitability increases of up to 30% and cost reductions of 30–40% by 2030.

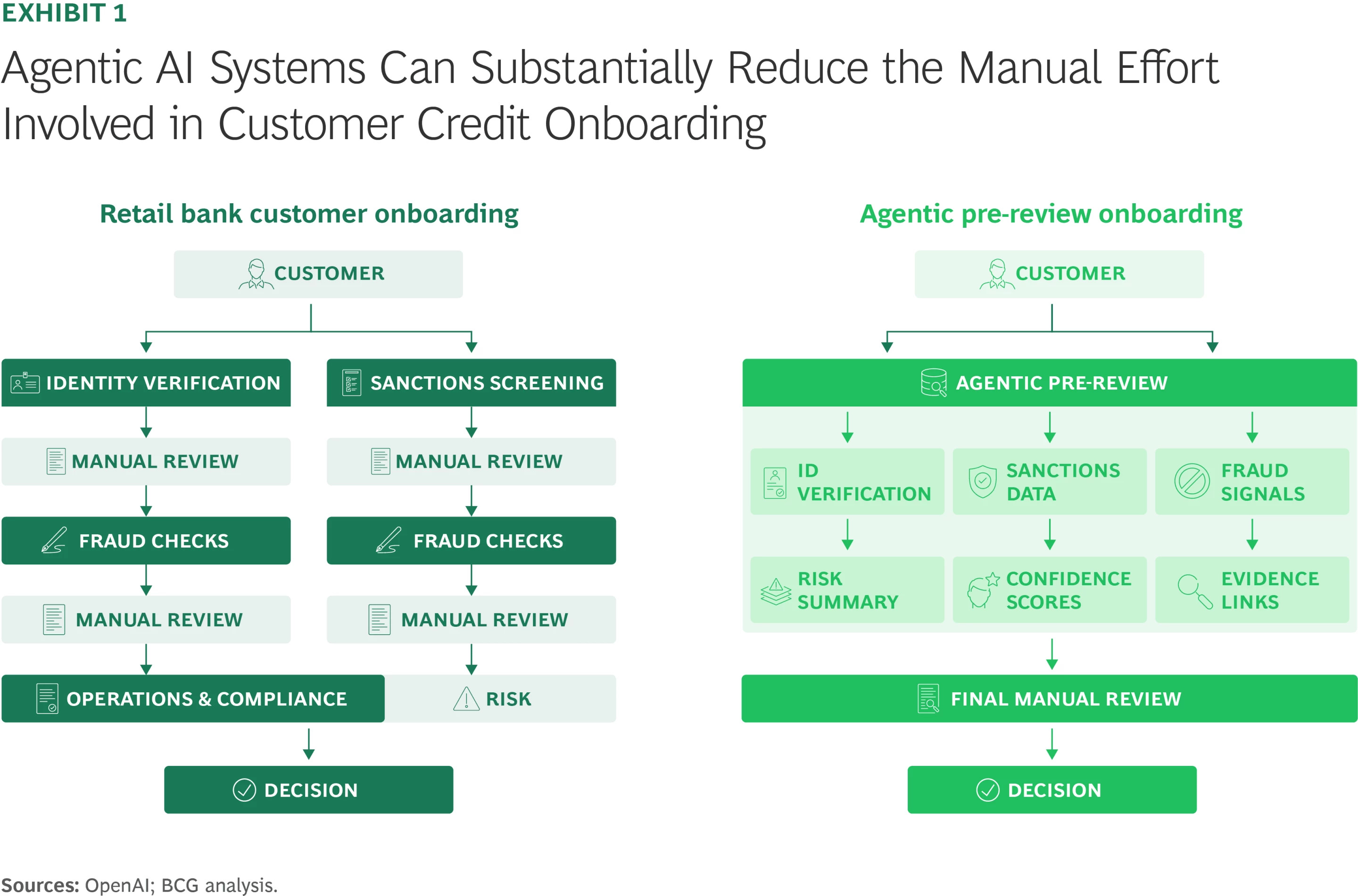

• The lending process remains structurally inefficient. Even after digitalization, banks still rely on human intervention to reconcile fraud checks, sanctions lists, and credit bureau data. This adds cost and time without improving risk outcomes. AI agents can generate structured and auditable pre-analysis summaries within existing policy frameworks.

• The back office represents the real opportunity. Processes such as credit risk analysis and approval support, or compliance documentation, have resisted traditional automation.

• Governance will separate leaders from the rest of the market. Banks that build centralized control processes and rigorously test agent performance before deployment will scale faster and avoid

regulatory issues.

However, the path to scaling is not without challenges. Many banks remain stuck in the pilot phase, constrained by fragmented initiatives, governance concerns, and uncertainty. BCG and OpenAI emphasize that success will depend on a disciplined implementation approach—one that combines

technological innovation with robust oversight.

At the core of this approach is the concept of “evaluation-driven development,” which ensures that AI systems are rigorously tested on real-world tasks before deployment. In parallel, banks must invest in processes that standardize how AI applications are governed, monitored, and integrated at the organizational level. Together, these elements create the foundation for scalable, compliant, and trustworthy AI adoption.

Ultimately, the study addresses a fundamental question: what will differentiate leaders from the rest of the market in this new era? The report’s answer is unequivocal—speed and execution.

Banks that act early will not only capture immediate cost advantages, but will also build the capabilities, data assets, and operational discipline required to sustain long-term leadership.

The full report is available here.