An analysis conducted by a group of authors from Boston Consulting Group, including Balázs Kotnyek, Partner and Associate Director, and Zsófia Beck, Managing Director & Partner—both from the Budapest office—examines the current state of the renewable energy market, the challenges it faces, and possible solutions.

Renewable energy sources—primarily wind and solar—have achieved remarkable success over the past decade. By the end of 2025, they had become the largest source of electricity generation globally. The main barrier to their deployment used to be high costs, but this has now largely been overcome.

The next major challenge is no longer the expansion of renewable capacity at all costs, but rather increasing the flexibility of the energy system.

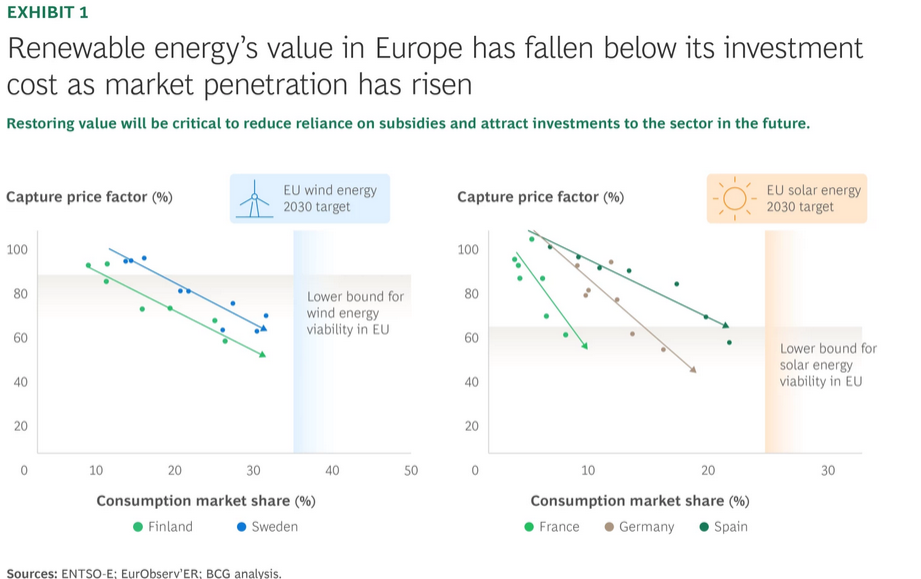

The core issue is that renewable sources typically generate electricity at the same time. When there is strong wind or intense sunlight, large amounts of electricity are fed into the grid simultaneously. When this coincides with low demand, prices drop sharply and may even become negative—meaning that producers must pay others to take the electricity. In other words, the very abundance of the technology reduces its value.

In several European countries, wind and solar producers can already sell their electricity only at prices well below the average wholesale level. The number of hours with negative prices has more than doubled within a few years. In the European Union, this resulted in €14 billion in lost revenue potential for producers in 2025. This situation may trigger a dangerous spiral: the faster renewable capacity expands, the greater the value cannibalization, and the less attractive new investments become.

The problem is further aggravated by the spread of distributed generation, such as rooftop solar panels. During the day, these systems not only cover household consumption but may also feed surplus electricity into the grid, thereby reducing demand for power from conventional plants twice over. In

addition, physical constraints in the grid—such as bottlenecks in the electricity transmission system—can prevent electricity from reaching where it is needed, creating local oversupply even when there is demand for renewable electricity at the system level.

Standard policy tools for renewable investments, such as subsidies and guaranteed purchase prices, provide only partial solutions. They can make individual projects financially viable, but overall they increase the total cost to society. The real solution lies in enhancing the flexibility of the entire power system—enabling electricity consumption, storage, and transmission to better adapt to variable generation.

Flexibility can be understood across multiple time horizons. Different tools are needed to manage fluctuations on the scale of seconds, days, or even seasons. In the short term—within seconds and minutes—accurate forecasting, smart grid operations, and fast-response technologies such as battery energy storage systems are essential. Batteries can also store electricity during low-price periods and feed it back into the grid during higher-price hours; however, this is currently economically viable only

within a single day, typically over a 4–8 hour period. This capability not only reduces price volatility but also increases revenues for renewable generators, as they can sell electricity to storage operators.

So-called virtual power plants are also becoming increasingly important.

These are digital platforms that aggregate and coordinate many smaller producers, consumers, and storage units—such as solar panels, industrial loads, or electric vehicles—and operate them as if they were a single large power plant. In this way, consumers and smaller producers can also become

active participants in maintaining system balance.

Medium-term flexibility—on the scale of days to weeks—is more challenging. Current storage technologies are either too costly or have limited capacity over such timeframes. Here, a larger role may be played by shifting industrial consumption over time, electrified heat production, and, in the longer term, potentially hydrogen production. However, this requires market rules that reward not only rapid response but also the availability of capacity over longer durations.

Periods with low wind and solar output—such as foggy November days—pose a particular challenge, as demand is high while renewable generation is low. In such situations, fossil fuel power plants typically step in, resulting in higher prices and increased carbon emissions. The system therefore

needs to manage not only excess electricity, but also shortages.

The example of Finland illustrates how flexibility can be developed in a deliberate and systematic way.

The share of wind power in the country has grown rapidly, leading to significant price volatility. In response, new market rules were introduced, forecasting was improved, and substantial battery storage capacity was installed. These measures have helped to mitigate intraday price fluctuations. As a result of multi-day periods of low or high prices, electric boilers have also spread rapidly. Connected to district heating systems, these units produce heat using electricity. When electricity prices are low, heat producers switch to electric boilers; during high-price periods, they switch back to biomass- or gas-based boilers. In this way, they support the balance of the power system and reduce the cost of heat production. It is therefore not surprising that by 2025, enough electric boilers had been installed to cover up to one quarter of the peak load of the entire electricity system.

BCG proposes several directions for the future:

• First, renewable investments should be planned not only based on installed capacity, but also on the value they create for the overall system. It is important that power plants generate electricity where and when it is most needed. For example, if solar panels are oriented more toward the west, they can produce more electricity in the afternoon and evening—when demand is higher—and less at midday, when there is already excess supply.

• Second, renewable generation should also be actively managed: in certain situations, curtailing production can be a rational decision.

This requires incentive systems to be designed in a way that does not reward producers for generating surplus electricity.

• Third, demand-side flexibility should be encouraged, for example through dynamic, time-of-use pricing in consumer segments that are able to adjust their consumption. Unlocking this flexibility depends less on large-scale investments or technological breakthroughs, and more on market coordination, communication, and well-designed economic incentives.

• Fourth, regulation and system planning must increasingly take both short- and long-term flexibility into account. Growing volatility increases the importance of rare but high-impact risks. The system-wide value of solutions that can address these risks—such as grid development or reserve capacities—is therefore rising.

The energy system of the future will, by its nature, be more volatile. The objective is not to eliminate this variability, but to manage it effectively.

Countries that succeed in transforming their energy systems will be those that not only build large amounts of renewable capacity, but also maximize the value of these resources within a flexible and integrated energy system.

The full analysis can be consulted here.