The total investment volume in Romania reached EUR 323 mln. in the first half of 2022, 6% higher compared with the amount transacted in the same period of the previous year, according to the Romania Real Estate Market Outlook 2022 research special report, launched by CBRE Romania, the leader of the real estate consultancy market.

In the first six months, 14 transactions were signed, with an average value of 23 million euros. At the same time, 79% of the year-to-date volume was concluded during the second quarter of the year. The largest transaction of the year to date was signed in the second quarter of the year, with the acquisition of EXPO Business Park by S IMMO AG from Portland Trust, assisted by CBRE.

Claiming the largest share of the total investment volume, Bucharest attracted 10 transactions. Only 20% of the total investment was directed towards regional cities out of which Cluj-Napoca emerged as the most sought-after regional location.

From the point of view of the market sectors, the office sector occupies the first position, with 62% share from the H1 2022 overall country investment volume. Industrial claims 15% and retail properties represents 12% from the total volume, while

hotel and mixed-use properties have a joint share of 11%, according to CBRE Research.

Regarding the nationality of the investors, the most important part of the capital, 37% of the total investment volume, was brought by Austrians, followed by Belgians (22%) and Romanians (18%). In the first quarter of 2022, the source of capital was exclusively foreign, Romanian investors closing several deals in Q2.

With investment deals pipeline quite consistent, the year’s total investment volume could surpass the 2021 volume. The pipeline of investment deals will be defined by the leasing market, combined with the ongoing outlook for financial conditions in the broader monetary markets.

With investment deals pipeline quite consistent, the year’s total investment volume could surpass the 2021 volume. The pipeline of investment deals will be defined by the leasing market, combined with the ongoing outlook for financial conditions in the broader monetary markets.

”The pipeline of activity for 2022 remains very strong and we are certainly seeing the premises for one of Romania’s strongest years in terms of transactional volume. The outlook for 2023 is more mixed, as the ongoing interest rate hikes are having a downward effect on liquidity. Even in this context, Romania’s high yields by regional standards are acting as a buffer to safeguard activity.” says Mihai Pătrulescu, Head of Investment Properties at CBRE Romania.

”The pipeline of activity for 2022 remains very strong and we are certainly seeing the premises for one of Romania’s strongest years in terms of transactional volume. The outlook for 2023 is more mixed, as the ongoing interest rate hikes are having a downward effect on liquidity. Even in this context, Romania’s high yields by regional standards are acting as a buffer to safeguard activity.” says Mihai Pătrulescu, Head of Investment Properties at CBRE Romania.

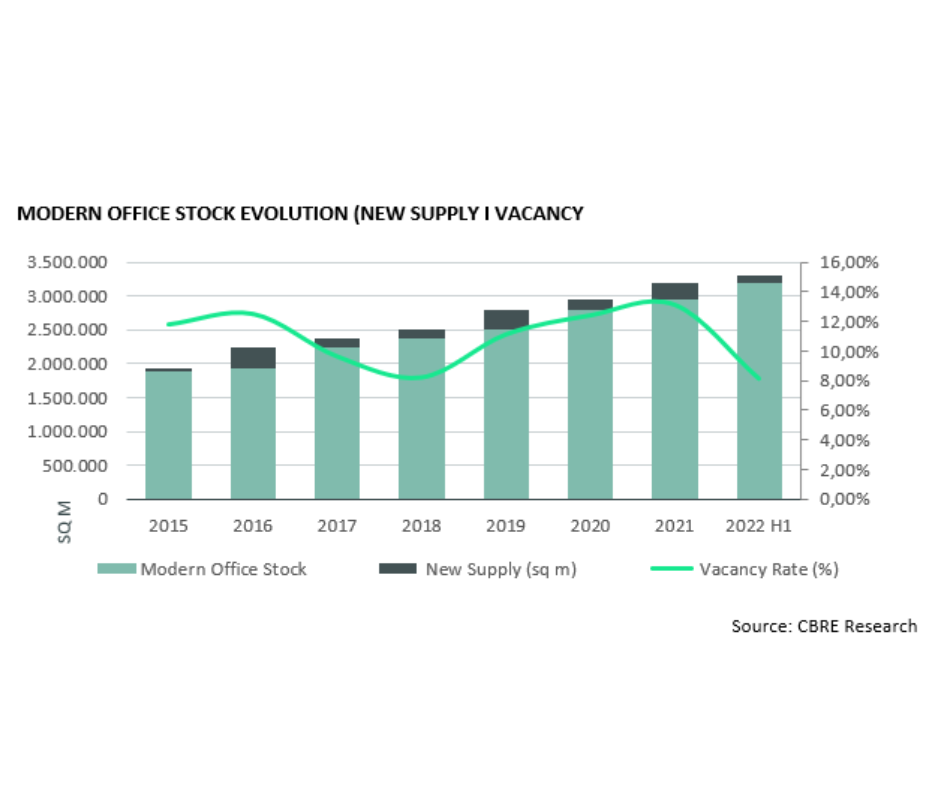

Bucharest modern office stock reached 3.30 mln. sq m at the end of first half of 2022, as four office projects with approximately 100,000 leasable sq m were delivered. The Center-West area of the city represents almost 60% of the new supply, as two projects – Sema Park II – Oslo & London building (31,500 leasable sq m) and AFI Tech Park 2 (24,500 leasable sq m) – were added to stock. At the same time, the Center and North-West sub-markets include two new deliveries, Tandem and the first phase of @Expo.

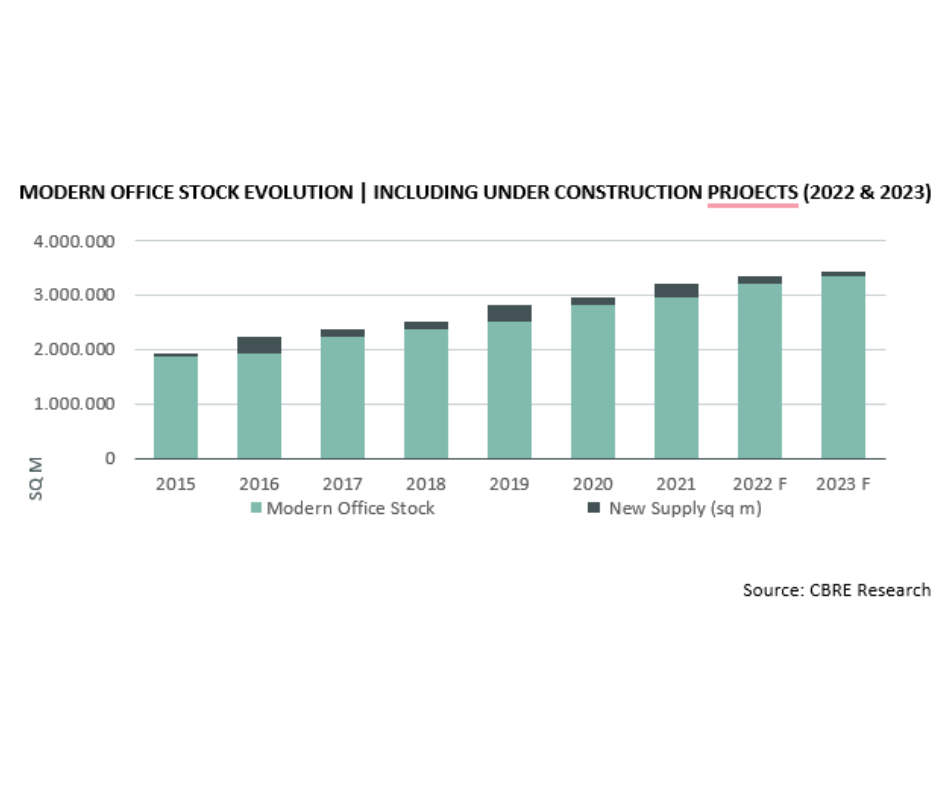

Moreover, another 41,400 sq m in two office buildings will be added to modern stock by the end of the year. 83% of the total area to be delivered will be added to the Center-West area’s stock, in one building, One Cotroceni – phase 2, with a GLA of 34,500 sq m. The remaining 17% is claimed by Center sub-market which will welcome Tudor Arghezi office scheme, a 7,000 leasable sq m project. At the same time, the Capital city’s modern office stock will have another approx. 94,000 sq by the end 2023.

Between January and June, the total office leasing activity in Bucharest reached 132,500 sq m, 18% higher compared with the same period of 2021. The total transactions excluding renewal/renegotiation represented 70% of the total leasing activity and was with 60% higher compared with H1 2021. The largest transaction was concluded by Booking Holdings, which leased 9,000 sq m in U-Center Campus phase 1. Another important transaction is the lease of 6,500 sq m in Immofinanz’s office building, Victoria Park by Leventer Hospital.

Regarding pre-leases, the largest deal was concluded in Q1 2022 by the iGaming software supplier, EveryMatrix, which secured 7,500 sq m in the Center office sub-market. Renewal/renegotiation transactions accounted for 38,100 sq m, with 16,600 sq m less than the amount renegotiated during the same period of 2021.

Regarding pre-leases, the largest deal was concluded in Q1 2022 by the iGaming software supplier, EveryMatrix, which secured 7,500 sq m in the Center office sub-market. Renewal/renegotiation transactions accounted for 38,100 sq m, with 16,600 sq m less than the amount renegotiated during the same period of 2021.

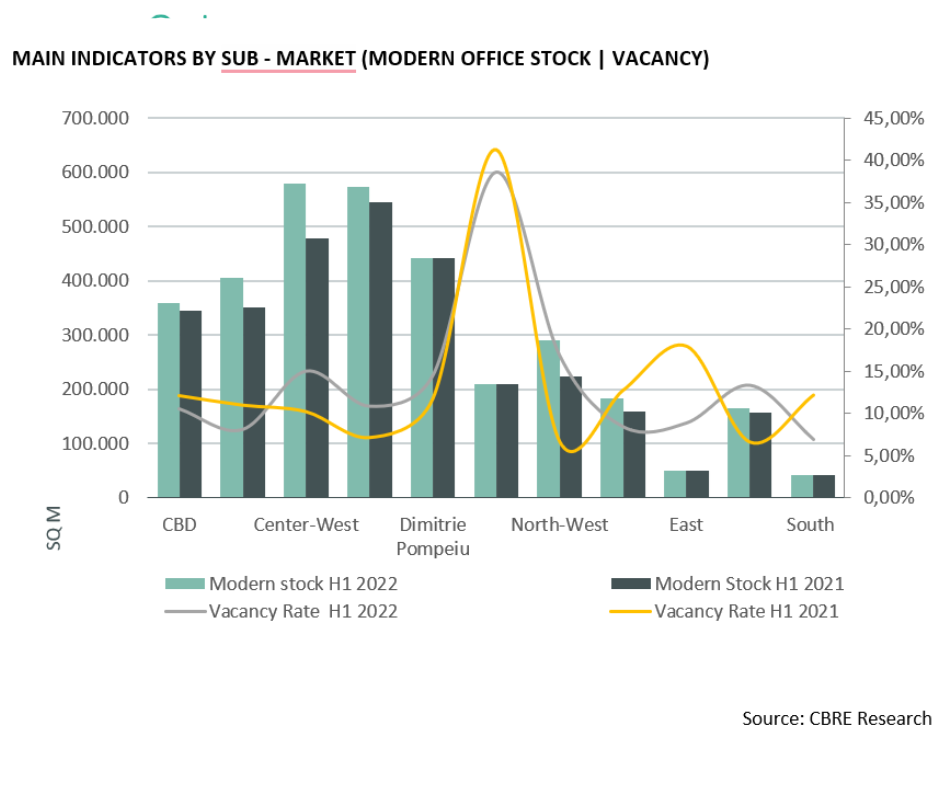

With 25%, 22% and 21% from the total leasing activity, Center, Center-West and Floreasca / Barbu Vacarescu are the top three office sub-markets. Next are the CBD sub-markets with a percentage of 17%, followed by Baneasa – Otopeni, South, North -West, Dimitrie Pompeiu and Pipera North office areas (15% from total leasing activity).

With 25%, 22% and 21% from the total leasing activity, Center, Center-West and Floreasca / Barbu Vacarescu are the top three office sub-markets. Next are the CBD sub-markets with a percentage of 17%, followed by Baneasa – Otopeni, South, North -West, Dimitrie Pompeiu and Pipera North office areas (15% from total leasing activity).

”The office market is entering a new era of development shaped by recent market dynamics and limited future supply. The work balance between home and office is still to reach consistency, but this adaptative way of working coupled with the leasing’ flight for quality enables the office market to reinvent itself in the mission to keep the leasing activity on an upward movement”, says Tudor Ionescu, Head of A&T Services Office at CBRE Romania.

”The office market is entering a new era of development shaped by recent market dynamics and limited future supply. The work balance between home and office is still to reach consistency, but this adaptative way of working coupled with the leasing’ flight for quality enables the office market to reinvent itself in the mission to keep the leasing activity on an upward movement”, says Tudor Ionescu, Head of A&T Services Office at CBRE Romania.

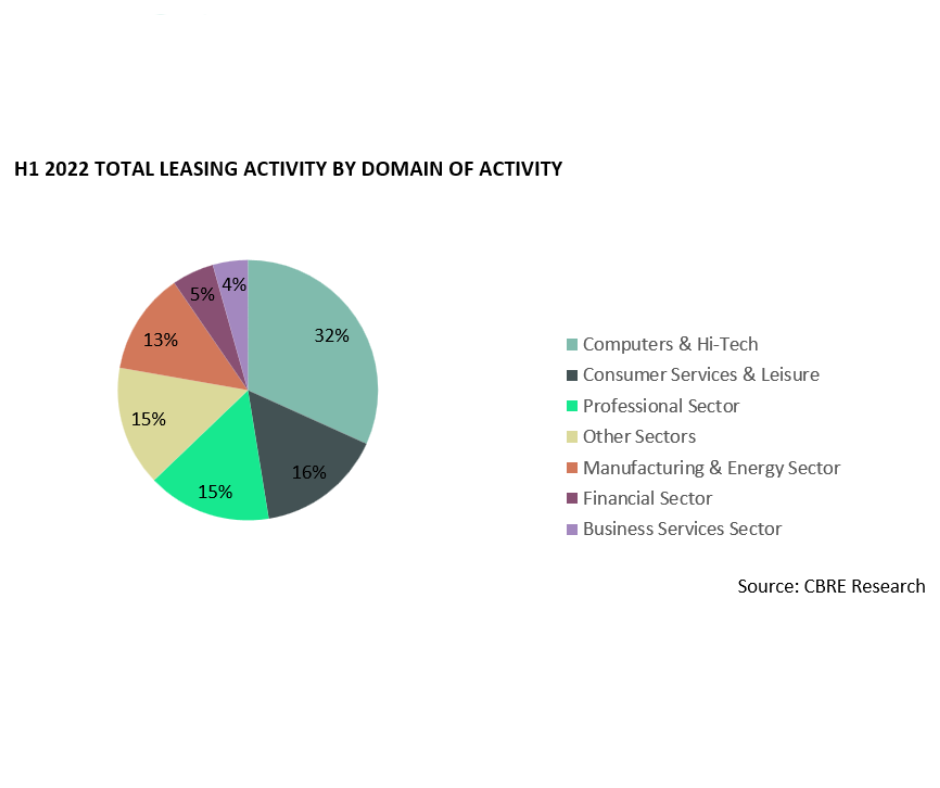

In terms of demand, Computers & Hi-Tech sector leads the market, with 32% of the total leased area in the first six months of 2022, followed by Consumer Services & Leisure (16%) and Professional (15%) sectors.

At the end of Q2, Bucharest modern office stock recorded a vacancy rate of 13.9%, similar with the level from the end of the previous quarter. When analyzing exclusively class A office schemes, the vacancy rate drops at 11.7% at H1 2022.

At the end of Q2, Bucharest modern office stock recorded a vacancy rate of 13.9%, similar with the level from the end of the previous quarter. When analyzing exclusively class A office schemes, the vacancy rate drops at 11.7% at H1 2022.

Starting with the first months of the year, prime rent increased with 0.25 EUR / sq m/month, remaining stable at the end of Q2, at 19.00 EUR / sq m/month. Landlords continue to show flexibility when negotiating incentive packages and lease terms, lowering the net effective rent. Nonetheless, the limited office pipeline for the short – term and the recorded leasing activity recovery which embarked on an upward path, could be the signs that indicate a mild transition towards a landlords’ market.